Will 2026 be the year more people start buying homes again? Experts disagree. Some predict home sales will grow by just 1.7%, while others expect 14% growth. That’s a huge difference, and it shows the big question everyone is asking: will slightly lower mortgage rates finally get people buying and selling again?

Almost all experts agree the housing market will be busier than 2025. But they don’t agree on how much busier. The National Association of Realtors thinks sales will jump 14%. Realtor.com thinks they’ll only grow 1.7%. Both might be right for different areas and price ranges.

If you’re planning to buy or sell a home in 2026, these predictions matter less than understanding what’s actually happening. Mortgage rates should drop a little. More homes will be available. Prices will keep going up, but more slowly. The market is starting to unfreeze. 🥶 Most importantly, the housing market is returning to more normal conditions after the wild ups and downs during COVID.

What Happened in 2025: Why the Market Stayed Frozen

The 2025 housing market was disappointing. Mortgage rates stayed above 6.5%, which kept many buyers away and meant very few homes were sold. By mid-2025, more than 80% of homeowners had mortgage rates below 6%. This created a “lock-in effect” where people didn’t want to sell because they’d have to get a new mortgage at a much higher rate.

Buying a home became really hard for most people. The typical first-time buyer was now 40 years old, not younger like in the past. This happened because monthly payments were too high for younger buyers. The market didn’t crash, but it didn’t get better either. Very few people were buying or selling.

2026 Predictions: What Experts Agree and Disagree About

Mortgage Rates: Most Experts Agree They’ll Drop Slightly

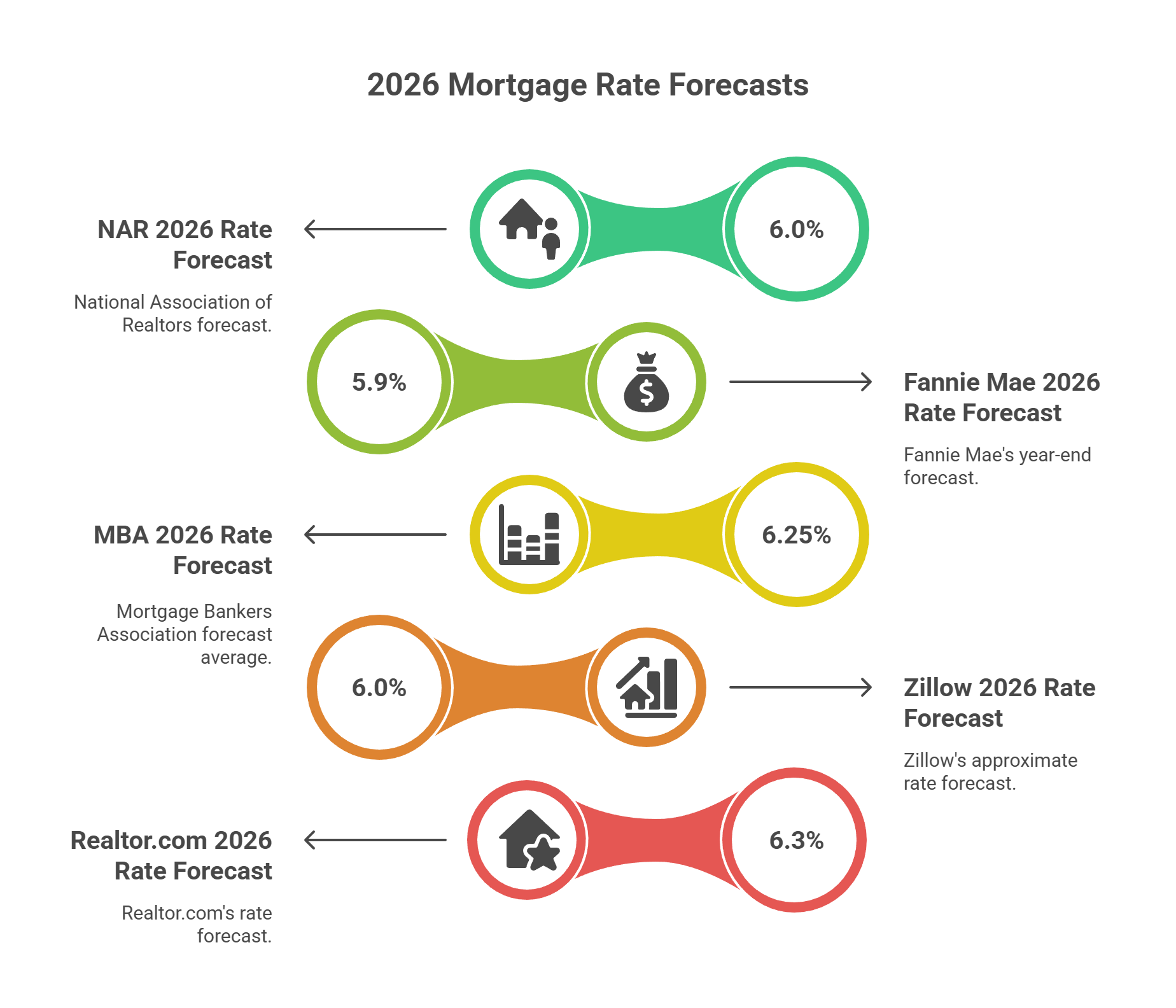

Most experts agree on where mortgage rates are heading. They expect rates between 6.0% and 6.4% in 2026, which is better than 2025 but still high compared to a few years ago.

2026 Mortgage Rate Predictions

- NAR: 6.0%

- Fannie Mae: 5.9% (end of year)

- MBA: 6.0% to 6.5%

- Zillow: around 6.0%

- Realtor.com: 6.3%

These similar predictions mean experts see the Federal Reserve making similar decisions. While 6% is still high compared to recent years, it’s better than what we had in 2025.

The real question is whether this small drop will actually get buyers moving. A drop from 7% to 6.5% won’t help much if buyers keep waiting for 5% rates or if sellers stay locked in at 3%. The National Association of Realtors estimates that a drop to 6% could bring 5.5 million more buyers into the market, including 1.6 million renters. But experts disagree about how many people will actually buy, which shows there’s real uncertainty.

Home Sales: Nobody Knows for Sure

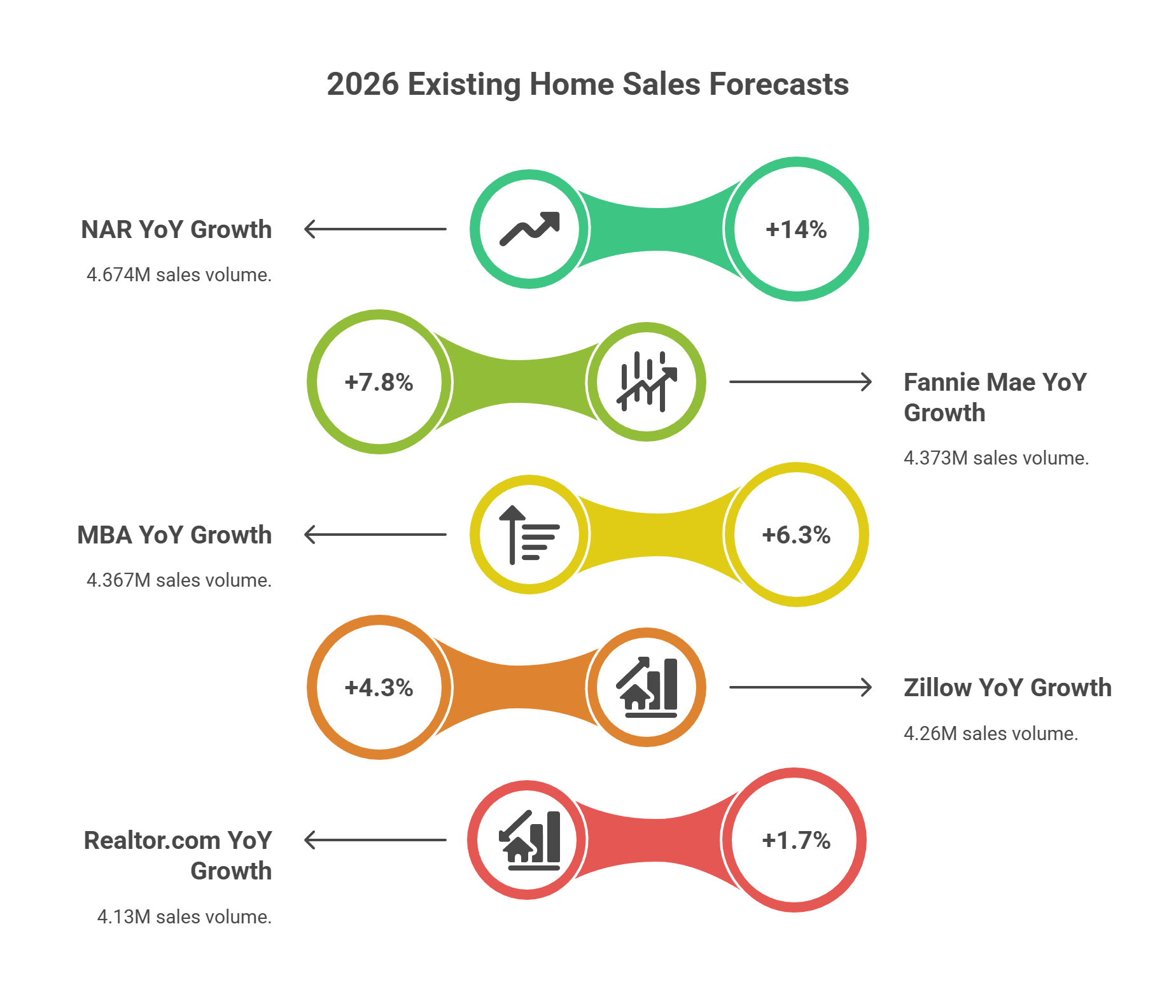

Predictions for how many homes will sell in 2026 vary much more than mortgage rate predictions. This shows that experts have different ideas about how fast the market will unfreeze.

2026 Home Sales Predictions

- NAR: 4.674 million homes (+14% from 2025)

- Fannie Mae: 4.373 million homes (+7.8%)

- MBA: 4.367 million homes (+6.3%)

- Zillow: 4.26 million homes (+4.3%)

- Realtor.com: 4.13 million homes (+1.7%)

This huge range from 1.7% to 14% growth shows real uncertainty about what buyers and sellers will do. Will homeowners with 3% mortgages finally accept that 6% rates are the new normal? Will life changes like new jobs, growing families, or divorces finally matter more than keeping a low rate?

What happens depends on several things working together. The lock-in effect needs to keep weakening. As long as many homeowners have mortgages way below current rates, they’ll stay put. But this will slowly change as more homeowners reach a point where life circumstances matter more than their rate.

Buyers also need to stop waiting for rates to drop back to the super-low levels of 2020 and accept that 6% is normal now. Many buyers spent the last two years waiting for big rate drops. But with 6-7% becoming normal and rates expected to drop a bit more, buyers may decide to jump back in.

Jobs and wages also matter a lot. Strong employment and rising wages give buyers confidence and the money they need to buy. Several experts expect home prices to grow more slowly while wages keep rising, which will gradually make homes more affordable in 2026. If jobs get worse, sales will likely be on the lower end of predictions. If jobs stay strong, sales will be higher.

Even small changes in interest rates or buyer confidence could make actual sales very different from predictions. This wide range shows real uncertainty about how people will behave, not just disagreement about the economy.

Home Prices: They’ll Keep Going Up

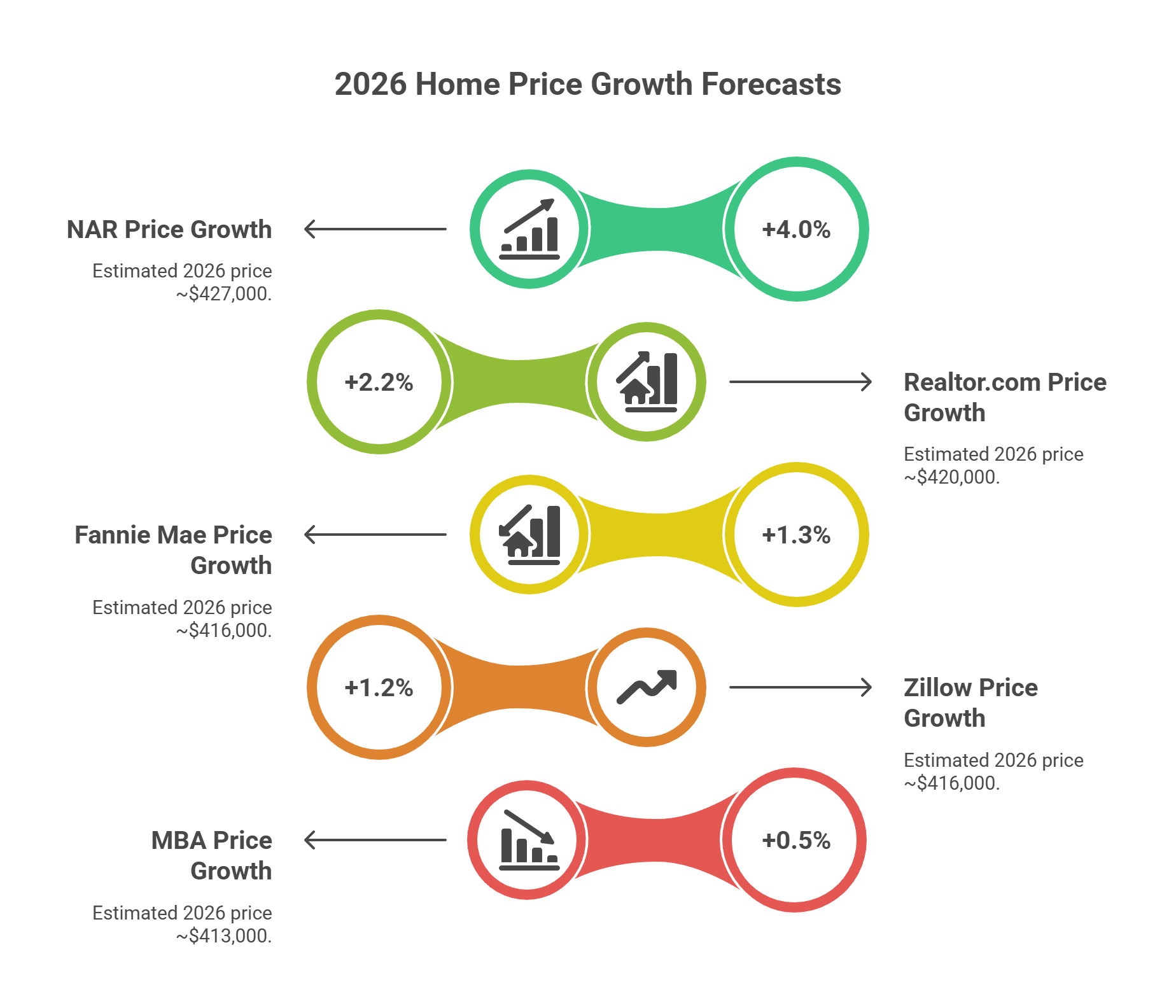

All major experts predict home prices will keep rising in 2026, though most predictions are between 0.5% and 4% growth.

2026 Home Price Growth Predictions

- NAR: +4.0% (around $427,000)

- Realtor.com: +2.2% (around $420,000)

- Fannie Mae: +1.3% (around $416,000)

- Zillow: +1.2% (around $416,000)

- MBA: +0.5% (around $413,000)

Based on mid-2025 median price of $410,800

Experts agree more on prices than on sales, which suggests they’re more confident about price direction. While they’re not sure how many homes will sell, they do think supply and demand will keep pushing prices up.

There still aren’t enough homes available compared to how many people want them. This has been true for years because we haven’t built enough homes. These supply problems continue to support prices even though fewer homes are selling.

Most homeowners are in good financial shape, with a lot of equity built up over recent years. This means fewer people need to sell in a hurry, and many buyers moving up can use their equity for down payments. This helps keep prices strong, especially for more expensive homes.

The expected price growth for 2026 is modest compared to recent years. These predictions show a return to more normal growth rates, not the huge increases we saw during COVID.

What This Means for Buyers

If you’re thinking about buying a home in 2026, you face a complex situation. You need to think carefully about affordability while accepting that waiting might not make things much better.

Accepting the New Rate Reality

Mortgage rates are expected to be between 6.0% and 6.4% in 2026. That’s better than 2025 but still way higher than during COVID. Rates below 3% happened because of emergency actions during the pandemic and probably won’t come back soon. If you’re waiting for rates to drop to 4% or 5%, you may need to adjust your expectations. Current predictions suggest low-to-mid 6% rates are closer to the new normal. Planning your purchase around these rates makes more sense. You can always refinance later if rates drop more.

More Homes to Choose From

While there still aren’t as many homes available as there should be, there are more options now than in recent years. This gives you more choices and flexibility. Homes stay on the market longer now, bidding wars are less common, and sellers are more open to contingencies, repairs, and price breaks. Competition is still tough for well-priced homes in good locations, especially in spring and summer. But overall, the market is less crazy than during COVID.

Pricing and Competition

Home prices are still expected to rise a little, with predictions from 0.5% to 4% growth nationwide. This means waiting might not lead to lower prices, even as rates improve slightly. However, slower price growth means less pressure and you can be pickier. Homes priced right should still sell, but overpriced homes now carry more risk because buyers have more choices. The market now rewards patience, preparation, and smart offers rather than just moving fast.

First-Time Buyers Face Big Challenges

First-time buyers still have the hardest time in 2026. The typical first-time buyer is now 40 years old, which shows how affordability problems, high down payments, and high mortgage rates have delayed homeownership for many people. Even with small improvements in rates and inventory, upfront costs and monthly payments are still big barriers, especially for buyers without existing equity.

That said, things may get slightly easier compared to 2025. Slower price growth and small rate drops reduce some pressure. More homes available means more choice and less competition. Low-down-payment programs, buying with family or friends, and looking in more affordable areas can help. While first-time buyers still face real challenges, the 2026 market offers more flexibility and less urgency than during COVID, making preparation and strategy more important than speed.

What This Means for Sellers

If you’re thinking about selling your home in 2026, market conditions are still generally good, but not for everyone equally. Results increasingly depend on location, price range, and your home’s condition. Well-priced, move-in-ready homes in desirable areas continue to attract strong interest. But overpriced homes or those needing a lot of work face longer selling times and tougher negotiations.

Thinking About Your Mortgage Rate

The lock-in effect still influences whether people sell, but the calculation is about more than comparing a 3% mortgage to a new 6%+ loan. Many homeowners now have a lot of equity that can offset higher borrowing costs, especially if you’re downsizing, moving to a cheaper area, or reducing your housing expenses. Life events like job changes, family needs, or retirement are increasingly mattering more than rate differences as sellers realize that rates in the low-to-mid 6% range are here to stay.

Pricing Your Home Right

Accurate pricing is critical. Overpricing increases the risk your home will sit on the market for a long time, which can make buyers suspicious and force you to lower the price anyway. Buyers in 2026 are more patient and better informed, with more alternatives than in recent years. You should use recent sales of similar homes and current local conditions rather than peak COVID prices. Homes priced correctly from the start are more likely to sell quickly and close to asking price.

Offering Concessions Is Normal Now

Since buying a home is still expensive for many buyers, seller concessions are playing a bigger role in successful sales. Closing cost credits, rate buydowns, and repair allowances are increasingly used to close deals without cutting the headline price. These tools let sellers stay competitive while helping buyers manage monthly payments and upfront costs. In many markets, concessions aren’t a sign of weakness but a practical response to current financing realities.

Preparation Matters

With more homes available than in recent years, how your home looks matters again. Homes in excellent condition get more interest and higher prices. Properties needing repairs are more likely to sit on the market. Small improvements like fresh paint, fixing deferred maintenance, professional cleaning, and quality photos can make a real difference. Pre-listing inspections can also reduce surprises during the sale and improve buyer confidence. In a more balanced market, preparation often determines whether your home sells quickly or requires multiple price cuts.

What This Means for Renters

If you’re renting in 2026 by choice or necessity, the decision is mostly practical. While rent increases have slowed in many areas, homeownership costs remain high due to prices and mortgage rates in the low-to-mid 6% range. In most of the country, renting continues to offer lower monthly costs and more flexibility, especially if you don’t have substantial savings or aren’t sure how long you’ll stay.

The rent-versus-buy decision in 2026 depends heavily on location, finances, and how long you plan to stay. Modest home price increases suggest waiting might not result in lower purchase prices. But renting can still make sense if you want flexibility or want to avoid overextending financially. Owning builds equity and stabilizes long-term housing costs. Renting preserves your options in a market still adjusting to higher rates.

For renters who want to buy eventually, 2026 may be best viewed as a preparation period. Improving credit, building savings, reducing debt, and watching target markets can significantly improve your future buying power. For others, continuing to rent remains a smart choice, not a failure to time the market right. In a market defined by returning to normal rather than big disruptions, making housing decisions based on your personal situation matters more than forcing yourself to buy.

Conclusion: A Market Returning to Normal

The 2026 housing market is defined less by dramatic change than by gradual normalization. Mortgage rates are expected to stay in the low-to-mid 6% range. Sales activity may improve modestly. Home prices are projected to rise at a slower, more historically typical pace. The wild swings of the COVID era have faded, replaced by a market driven more by income growth, supply constraints, and household needs.

For buyers, sellers, and renters, success in 2026 depends less on timing the market perfectly and more on adapting to it. Buyers get more choice and negotiating power but face ongoing affordability challenges. Sellers still benefit from limited supply, but pricing discipline and preparation matter more. Renters continue to balance flexibility against long-term ownership goals. With rates unlikely to return to COVID lows and prices expected to hold steady, the market rewards realistic expectations, financial readiness, and decisions based on personal circumstances rather than predictions of dramatic shifts.

Sources

- Realtor.com – Housing Forecast 2026

- NAR Real Estate Forecast Summit

- RealtorMag – Mortgage Rates Below 6 Percent

- National Association of Realtors – First-Time Home Buyer Report

- Zillow – 2026 Housing Predictions

- MBA – Mortgage Forecast

- Fannie Mae – Economic and Housing Outlook

- NAR – Existing Home Sales Report

All information on this site is deemed reliable, but not guaranteed. Do your own Due Diligence and consult a professional Realtor like Libby Guthrie.

Leave a Reply